Have you ever come across an investment opportunity so good that it feels it can only happen once in a lifetime?

Like you won’t have the chance to benefit from it again.

It happened to me twice in my life so far.

The goal is not to just brag about investment opportunities – if something, I feel more like I missed out. But it’s trying to understand the factors behind finding good deals and make the most out of them.

What are those qualities that turn an investment from promising to life-changing? The cool kids call them ‘moonshots’ or ‘100-baggers’.

Of course, what I call a moonshot might mean just another ‘good’ investment to a successful angel investor with a huge network.

Similarly, what I take for granted, generating enough passive income to achieve financial independence might be a mind-blowing fact to someone who’s just starting out.

Perspective is everything.

Moonshot #1

The first once-in-a-lifetime investment opportunity I came across appeared in 2016. A young startup was assembling a team ready to bring free stock investing to the masses. Yup, you guessed it right, I’m talking about FreeTrade.

Robinhood was already successful in the US and on the rise. FreeTrade appeared to be the wanna-be European version of that. And it did!

When FreeTrade opened the gates to crowdfunding, I was debating whether I should invest or not. Very challenging project but very rewarding if they can pull it off. Its share price started at £0.079561 a share.

And of course, they did manage to pull it off. Even without sneaky tactics like Robinhood.

Quarter by quarter, year over year, the app added new features, new users, and showed fantastic growth thanks to the early marketing moves of a talented individual, Viktor Nebehaj.

Without wasting any time, FreeTrade kept raising new funds from new crowdfunding rounds. This not only converted investors to real customers but they also became the biggest proponents of the FreeTrade movement. The world started to notice.

They offered a very good product and raised $15m Series A (Draper) and $69m Series B more recently.

The rest is history. The app has now over 1 million users and is expanding all over the world.

Here is the fundraising journey so far.

| Fundraise | Date | Share Price | Multiple (since round 1) |

|---|---|---|---|

| Round 1 | Sep-2016 | £0.079561 | 1x |

| Round 2 | Apr-2017 | £0.15311 | 1.9x |

| Round 3 | Jun-2018 | £0.521053 | 6.5x |

| Round 4 | May-2019 | £0.84324 | 10x |

| Round 5 | Aug-2019 | £0.956004 | 12x |

| Round 6 | May-2020 | £2.51 | 31x |

| Round 7 | Aug-2020 | £2.51 | 31x |

| Series B | Mar-2021 | £3.77 | 47x |

47x your initial amount in 4.5 years! Or “just” 50% in 1 year if you only invested in 2020.

I invested a small amount in the 2nd round and bigger sums in subsequent rounds. Definitely not enough! To be fair, I still find it reasonable not to fully trust a new product/new team that’s just starting out and only invest accordingly as you build confidence.

But another way to understand the opportunity better and build conviction is to join the team!

I could have tried to join the engineering team 5 years ago and truly understand them. That would require getting out of my comfort zone and changing gears. Being too comfy doesn’t move the needle!

Overall, a £10,000 investment in the first round would make you almost half a million 5 years later. And that’s all tax-free, part of the generous EIS scheme.

Moonshot #2

Regardless of how you feel about crypto, you can’t deny it has been a massive wealth creation engine in the past 7-8 years.

It used to be only engineers/tech bros. Then retail took notice in 2016 and the party started. Now we see bigger players and even institutions piling in and wanting a share of the pie.

We see big companies, like 5-billion market cap big, mining Bitcoin and listing on Nasdaq. Distributed teams build the Web 3.0 as we speak where no Facebook or Amazon will own your data or computing power.

They are backed by huge companies like Galaxy digital ($10bn market cap) and smaller players like KR1 ($400m).

Again, it doesn’t matter if you think crypto/DeFi/Web 3.0 is the ultimate innovation, digital gold or a massive Ponzi scheme. It’s actually sad that people think one or the other most of the time.

It doesn’t change the fact it has made some people extremely rich and qualifies as a once-in-a-lifetime opportunity in my book.

Even if you only put some money at the peak of the 2017 bubble or even as late as 2020 you’d still be sitting on gains in 2021.

Again, here, my approach was to dip my toes in something like this but not be really affected if it goes to zero. My matched betting history forced me to have some fun here and I’m glad I took some exposure in 2017.

Do you see the common themes here? That’s no way to exploit once-in-a-lifetime investments! Not to mention these belong to the past! What about the future?

How can I find the next big investment?

Let’s start with the factors I see as most important to find and assess those life-changing investments.

Position sizing is everything

You can brag all day you want about the 20-bagger but if it’s only turning £100 into £2,000 then that’s not making a big difference.

If I learned something from having some exposure to big percentage gains is that the amount you’re willing to commit is extremely important.

To put it simply, let’s say your goal is to earn £10,000 from investing.

If you invest £50,000, it takes a 20% return to earn £10k. To earn the same £10k with a £10k investment you would need a 100% return!

That’s a 5x higher return compared to the first case, or waiting 5x the time period (ok, ignoring compounding)!

A higher stake can turn a gain that pays for the next 2-week vacation into a quit-your-job-for-10-years kind of savings.

To clarify, I’m not necessarily talking about the pound amount but size as part of your overall portfolio.

Position size is very important. Just ask our own Monevator who “lost” £436,957 by reducing his Tesla position too early.

Concentrate Your Risk

Read any personal finance blog, including this one, and they’ll tell you to diversify. Don’t put all your eggs into one basket.

But you look at those investors who have made it big and you see concentrated risk, not diversified one. Like this hidden retail trader who made $7bn on Tesla by going all-in, and staying in.

Of course, I’m not suggesting we do that, but it really shows how position size and concentration affect the gains if the opportunity pays off.

Diversification is admitting “I don’t know, so I invest in everything and that’s good enough”.

But if you face a life-changing opportunity like the two above, why not go big? I know, I know, not all opportunities pay off and there’s some survivorship bias going on here.

You look at businessmen, like Felix Dennis of How to get rich book and they have one thing in common: They put most (if not all) of their assets into very few bets. They put all their eggs in there and then some!

Sometimes more than they have, either in a form of a loan or using other people’s money.

Not just their working capital, but their human capital too (i.e. their working hours).

Concentration pays if you are sitting on a big winner. Diversification pays if you’re wrong.

All things considered, having the right position is hard because hindsight is 20/20. But it’s what really matters when you’re winning.

Fish where the pond is less crowded

There are not many people who are willing to invest in something out of the ordinary. A small startup, an emerging asset class, a property in a lesser-known town.

Sometimes people/funds are not even allowed to invest even if they wanted to. Institutions have mandates and professionals have benchmarks they need to follow.

They also bear career risk. No professional will get fired for a 50% portfolio drop in 2008-09 because the entire US dropped. But fall 50% because you invested in Russia or something unconventional and you’re looking for a job.

However, retail investors don’t have that risk. They can wait for longer time horizons or invest without investment committees.

For example, in this excellent interview, Ari Paul told Raoul that a VC could not close funding because their custodian wouldn’t support the new token! Such limits are unheard of for smaller private individuals.

Ted Weschler, Warren Buffet successor at Berkshire recently made 450% in his personal account by investing in Dillard’s in 2020. He couldn’t have made the same investment at Berkshire without moving the needle, obtaining controlling interest etc. Dillard’s market cap is too small.

The bigger the firm or fund the harder it is to invest in smaller companies. The same goes for property investing.

For example, small retail investors like myself can buy the £500k buy-to-let down the street. Big players, not so easily!

To sum up, smaller investors can fish where the pond is less crowded 🙂

So looking for areas that other investors are not aware of is key here. Noone knew about cryptos before 2016. I am a software engineer. Thanks to some domain knowledge here I had heard of BTC before 2016. The crypto pond was completely empty.

How can we find those empty pond spots in the first place?

I’d say focusing on our circle of competence (Buffet style!) definitely helps to:

a) identify opportunities

b) better assess those opportunities

I happen to be between tech and finance, a usual suspect in tech meetups, pre-covid. Talking to people, seeing what’s out there I couldn’t have missed FreeTrade even if I wanted to.

Same goes for Mondo Monzo 😉

The same goes for spotting the trend of massive cloud adoption that happened in the early 2010s. It was a huge profit driver for companies such as Amazon, Microsoft, Google and more recently, Alibaba.

Finding the right opportunities means you’re already ahead of most people who are not in the domain or able to invest (country, regulations etc).

Exit timing matters

Everyone loves a good story but nobody loves the pain of having to go through the pain of holding your winners during tough times.

First of all, a successful trade requires you to be right twice. Buy the right time, sell the right time.

Sell too soon and you won’t let the opportunity ride to its full potential. That’s probably the hardest thing for me. How do you justify not selling when you’re up 500%?

Self-doubt kicks in. Anchoring kicks in.

- I’m too greedy

- Is this sustainable?

- Am I really willing to look wrong when others make money?

- Is this pure luck?

- Peer pressure to take some profits

Secondly, often the greatest opportunities come with much much pain. Look at very successful companies like Amazon or Tesla.

Amazon (-92% in 2001, -75% 2006, -64% 2008), Bitcoin (plenty of 50-80% every couple of years) and other once-in-a-lifetime opportunities.

It’s not easy to hold onto a winner during tough times. Buying is only half the battle.

This is why I don’t buy the ‘If you invested £1,000 in bitcoin in 2011‘ arguments. No!

You would have sold it a few years later when you thought a 10x return is pretty astonishing.

We are victims of our own success sometimes. We are anchored to the price we paid and view everything through that lens.

Anchoring bias is a cognitive bias that causes us to rely too heavily on the first piece of information we are given about a topic. When we are setting plans or making estimates about something, we interpret newer information from the reference point of our anchor, instead of seeing it objectively. This can skew our judgment, and prevent us from updating our plans or predictions as much as we should.

Example: I bought this house for £500k there’s no way I am selling it for the same amount, 10 years later. I want £1m and I’m willing to wait forever.

Personally, I believe the most important way to overcome anchoring bias is to ask myself: If I didn’t hold this investment, would I be willing to buy it at this price? If the answer is yes, it’s an easy hold, even after it has gone up by 5x since I bought it.

Overcoming anchoring bias allows you to average up! Not down. People who have made it tell us that one of the biggest lessons they learnt is to contribute more to their positions after big gains.

Alright.

In conclusion, if you want to find and capitalize on amazing investment opportunities, the above factors are the most important ones in my view.

This is also why passive investing is so powerful. You don’t need to worry about any of this. You just let the market do the worrying!

As a result, you have a less stressful journey and can focus on other things in life. I think most people are better off choosing a set it and forget it lazy portfolio of index funds.

This is what I do for the most part of my portfolio.

I won’t get rich quick, but I will surely get rich slowly.

Now tell me. What is YOUR once-in-a-lifetime investment? Or perhaps one you missed out on?

On another note, are you a business owner?

Registrations have just opened for the Company Investing Academy starting in January 2022.

If your company sits on idle cash earning no interest, I highly recommend the Company Investing Course starting in January 2022. There has never been a better time to learn how tax and investing works for limited companies.

Use coupon EARLYBIRD22 to get £100 off (valid until the end of November).

9 thoughts on “Moonshots”

What goes up tends to go up. Go in when you think you’ve missed out. (eg TSLA at 200$, BTC at 15k, etc).

Do you think the boat for crypto has sailed now? If not….where would someone start from here?

I sat too long in the “sounds like a dodgy scam to me” chair….

Read these articles on where it could go. You won’t be too late. https://planbtc.com/

With BTC and crypto, the answer is.. who knows! You’re definitely not early, but I don’t think you are late.

You’ll need a strong stomach to hold crypto through the winters though and be prepared to see your pot decline by 50-80% at times. There is no way to value it! BTC makes the same sense at $10k as at $100k. Not to mention the regulatory risks.

All these don’t make it necessarily a bad bet, just a very risky one! Starting small might show you how it feels like first-hand. As always, not financial advice and do your own research :)

I agree you need to take concentrated risk to really make it big. The trouble is you generally only hear about those that make it. Plenty more will lose, some even ruined.

Hey Michael, what is your opinion about the FED warning that valuations are high and there is a risk of correction? Do you plan to allocate on cash or other safe investments and what? Could do an article on that to share your thoughts! I’m not quite sure what to do at this point. We’ve been waiting for crash since 2015 at the end of the traditional 7 year market cycle.

Not an easy decision! Although it’s tempting to sell and fly to safety I would stick to my asset allocation. So if valuations are high and your assets have increased by a lot then maybe it’s time to rebalance.

That would mean selling the risky assets for riskless assets and when the tide turns do the opposite.

Predicting a crash can be sometimes successful but if you are too early then you might be worse off. And it’s usually in the final legs of a bull market that the biggest gains occur.

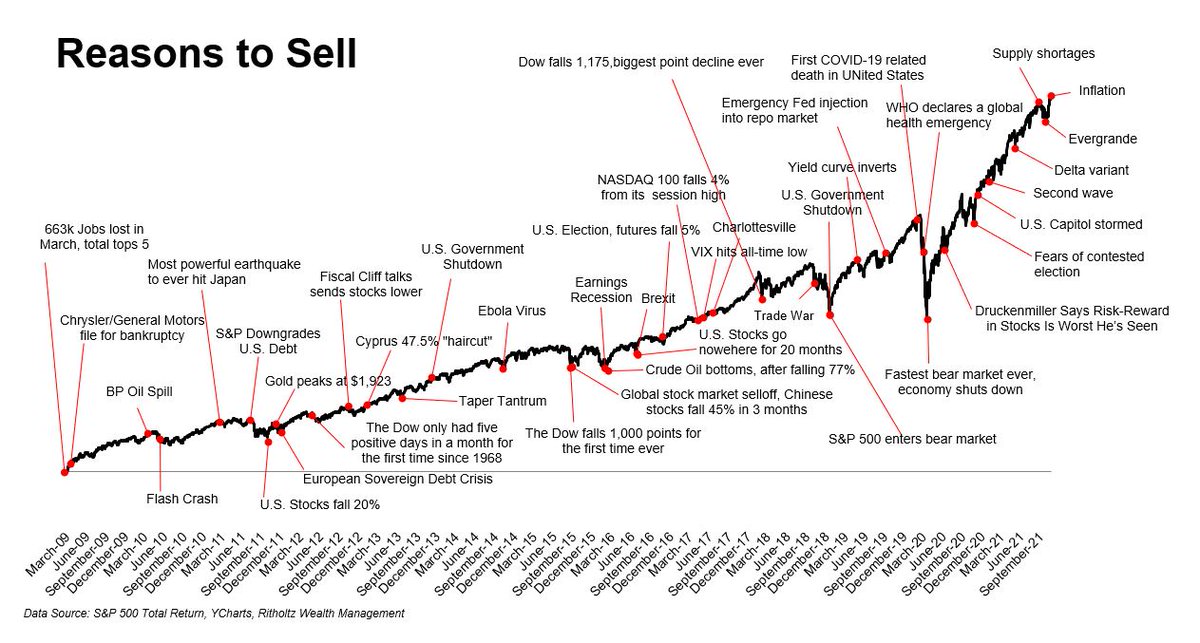

I found the ‘reasons to sell’ image by Batnick fascinating during one of the best decades in stock market history :)

This is a really thought provoking article. I’ve had a a small handful of moonshots over the last few years. In all cases my position size was way too small to be truly meaningful. I DCA’d on the way out, so hindsight shows I sold too soon, but no regrets trimming profits along the way.

Currently sitting on something that at its peak was 40x from my entry and now has declined to 10x. Still holding 25% of the original investment on the way down. Tough call to either sell and find greener pastures elsewhere and still bank a profit. Or hold on and hope it’s like Amazon and Tesla and bounces back eventually and resumes the run.

Those moonshots are messing with our psychology, aren’t they! I think it’s hard to re-assess the opportunities as the amounts grow so DCA is definitely a good way to better risk manage buying and selling.

Thanks for the thoughtful input, Thomas!